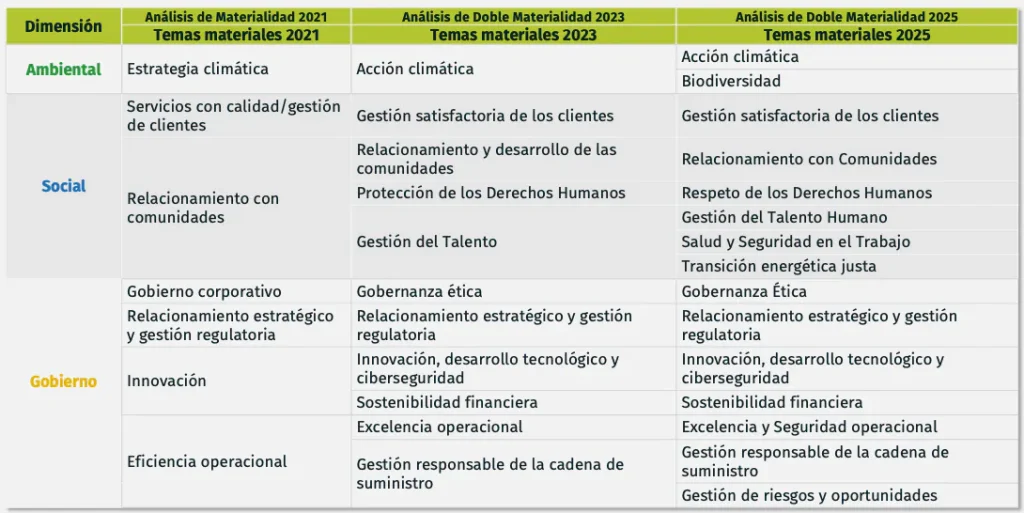

Línea de tiempo asuntos materiales

Sobre nuestra matriz

En línea con el propósito de mejorar vidas, transformar realidades y lograr prosperidad colectiva para todos, en 2025 la Transportadora de Gas Internacional S.A. ESP, llevó a cabo un proceso de revisión y actualización de sus asuntos materiales, en colaboración con la firma consultora Environmental Resources Management Colombia Ltda.

Este ejercicio se desarrolló siguiendo el modelo de Doble Materialidad, que abarcó dos perspectivas, una desde el enfoque financiero «de afuera hacia adentro» destinada a identificar nuevos y futuros riesgos que los asuntos Ambientales, Sociales y de Gobierno Corporativo (ASG) generan en la situación financiera, desarrollo, rendimiento y posición de la empresa, los cuales pueden influir en su valor y en la continuidad del negocio; y una perspectiva de impacto «de adentro hacia afuera» que evaluó de manera exhaustiva los impactos materiales, reales y potenciales, positivos y negativos, que TGI tiene en el entorno y sus grupos de interés a causa de sus operaciones.

Este análisis se ha llevado a cabo conforme a los requerimientos de la Superintendencia Financiera de Colombia a través de las circulares 031 de 2021 y 012 de 2022, así como los nuevos requerimientos de GRI (versión diciembre 2021).

Nuestro Análisis de Materialidad

Metodología

Etapas de la doble materialidad

Las etapas que se han llevado a cabo para la determinación de la doble materialidad son:

Definición de Asuntos Iniciales ASG

Materialidad de Impacto:

- Diagnóstico de los impactos potenciales positivos y negativos

- Evaluación de Impacto con Grupos de Interés priorizados

- Resultados de materialidad de impacto

Materialidad Financiera:

- Evaluación de los riesgos financieros

- Mapa de calor

- Resultados de materialidad financiera

- Indicadores con mayor impacto

Determinación de Doble Materialidad según criterios metodológicos y umbrales de calificación.

Identificación de temas y subtemas materiales

About The Materiality Matrix

In line with its purpose of improving lives, transforming realities, and achieving sharedprosperity for all, in 2025 Transportadora de Gas Internacional S.A. ESP (TGI) carried out a review and update process of its material topics, in collaboration with the consulting firm Environmental Resources Management Colombia Ltda.

This exercise was conducted following the Double Materiality approach, encompassing twoperspectives: a financial perspective (“outside-in”), aimed at identifying emerging and future risks that Environmental, Social, and Governance (ESG) matters may generate for thecompany’s financial position, development, performance, and overall condition, potentiallyaffecting its value and business continuity; and an impact perspective (“inside-out”), whichcomprehensively assessed the material, actual, and potential positive and negative impactsthat TGI generates on the environment and its stakeholders as a result of its operations.

This assessment was carried out in accordance with the requirements established by theColombian Financial Superintendence through Circulars 031 of 2021 and 012 of 2022, as wellas the updated GRI requirements (December 2021 version).

Material Topics Timeline

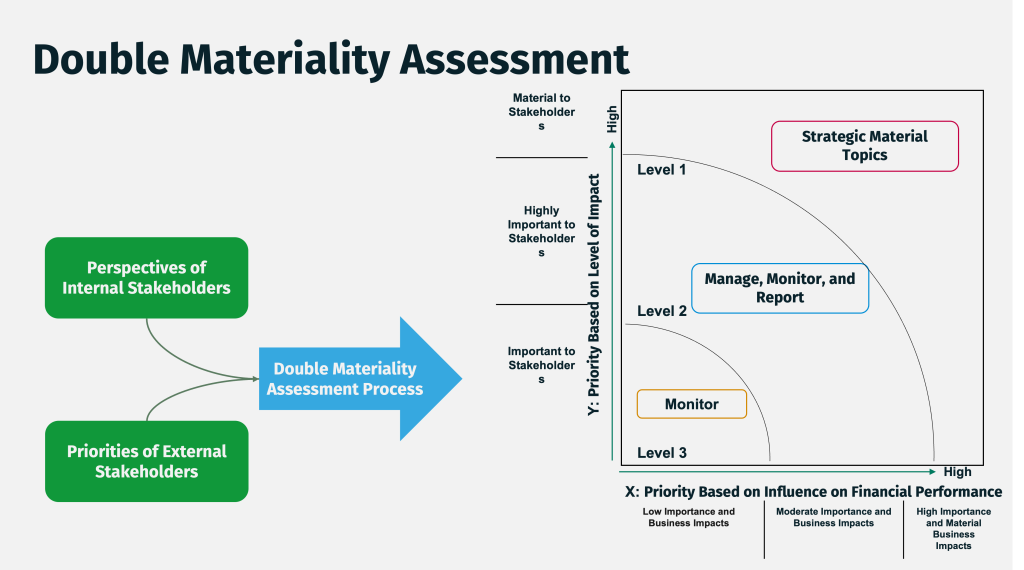

Double Materiality Assessment

The double materiality assessment integrates both impact and financialperspectives through an evidence-based and objective process to identifystrategic topics for TGI’s sustainability while also determining the topics that are most relevant for stakeholder engagement.

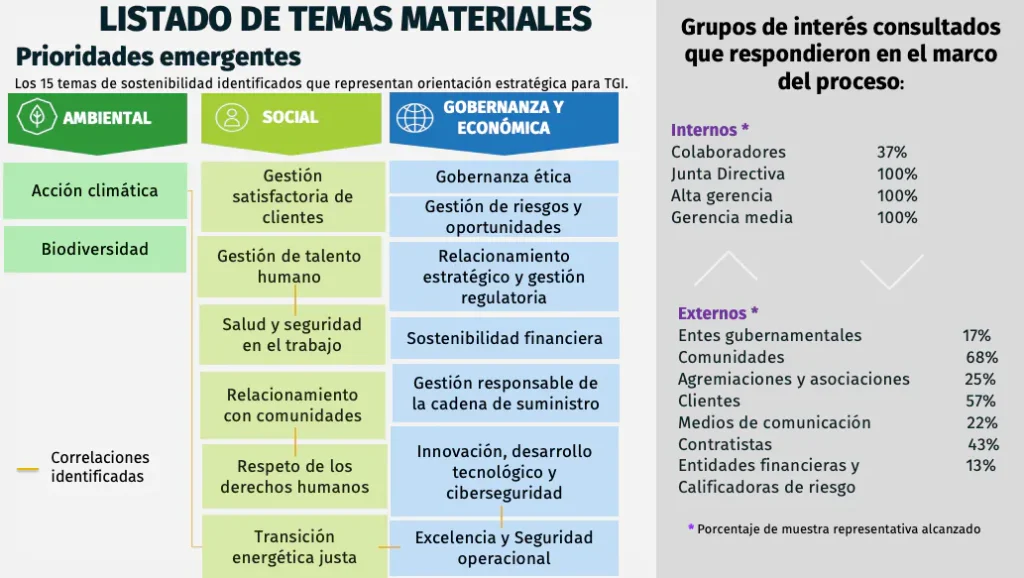

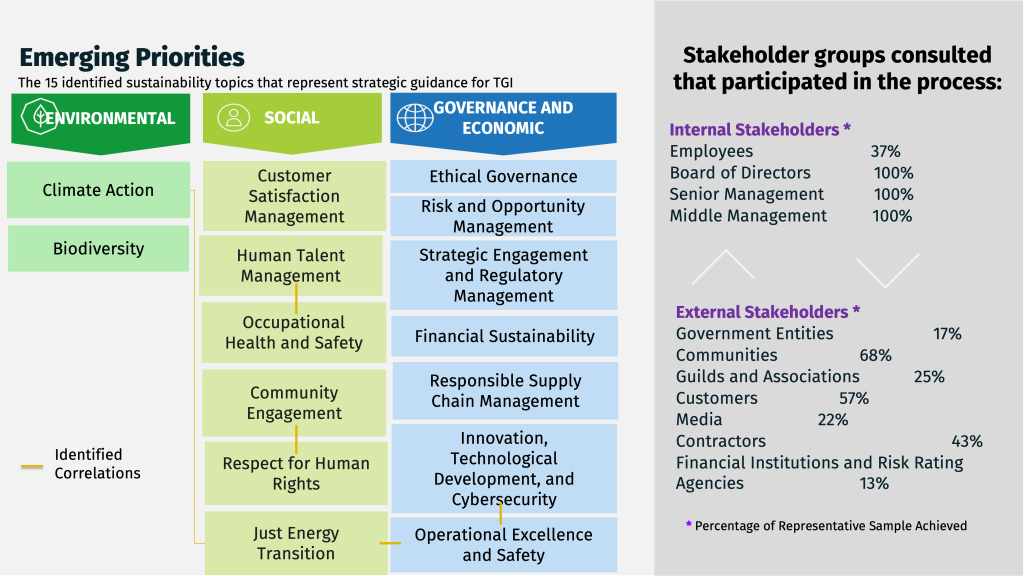

Emerging Priorities

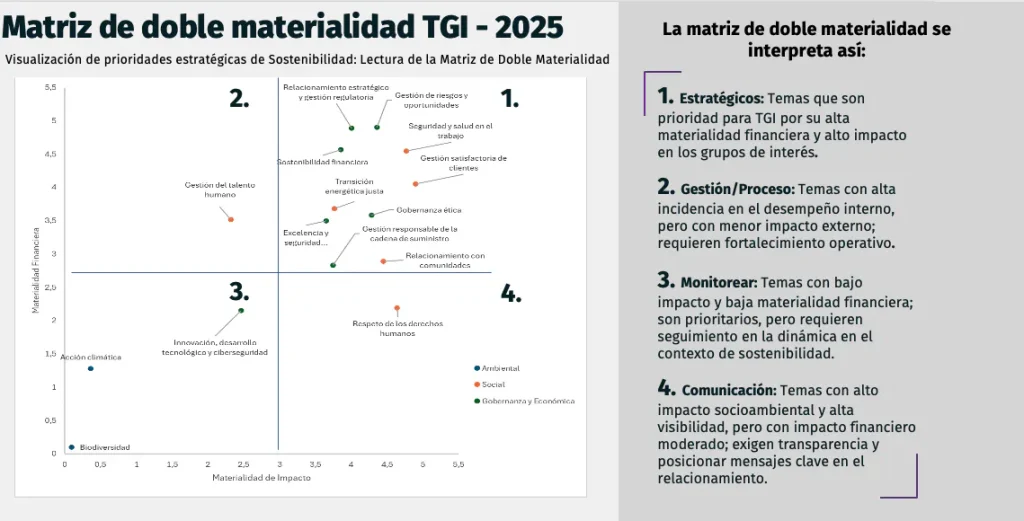

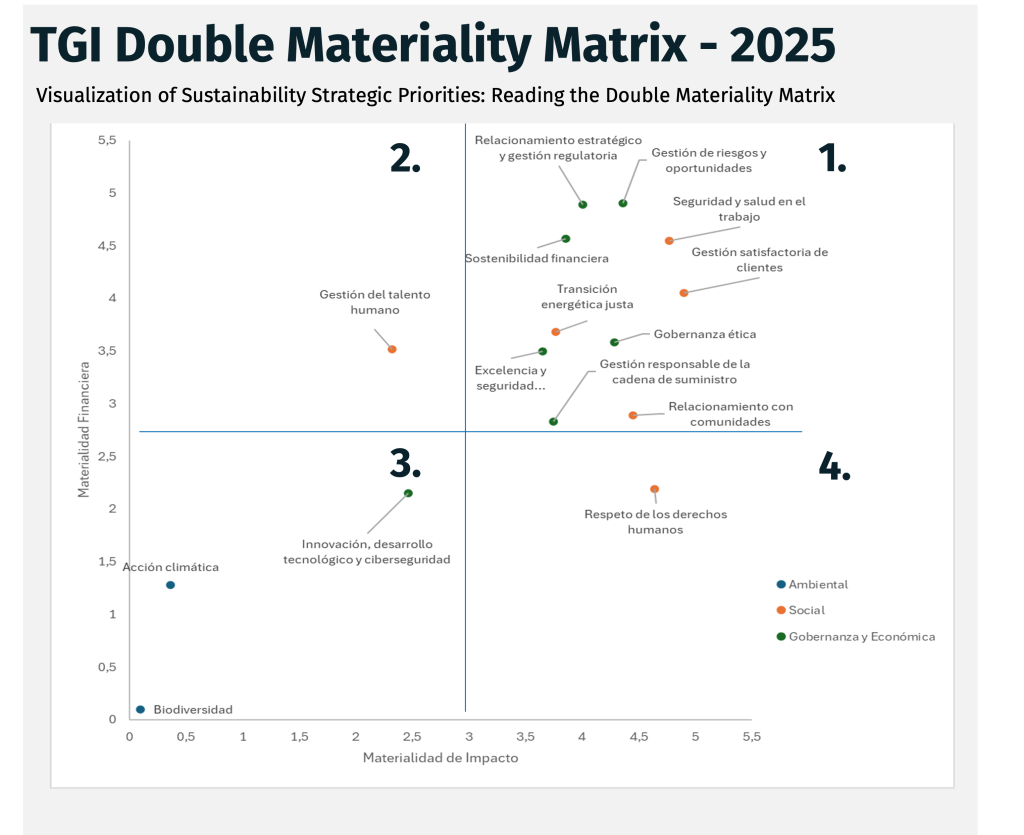

TGI Double Materiality Matrix - 2025

The Double Materiality Matrix is interpreted as follows:

- Strategic: Topics that are a priority for TGI due to their high financial materiality and significant impact on stakeholders.

- Management/Process: Topics with a high influence on internal performance but lowerexternal impact; these require operational strengthening.

- Monitor: Topics with low impact and low financial materiality; while they are notcurrently priorities, they require monitoring within the evolving sustainability context.

- Communication: Topics with high social and environmental impact and strongvisibility, but moderate financial impact; these require transparency and the positioningof key messages in stakeholder engagement.

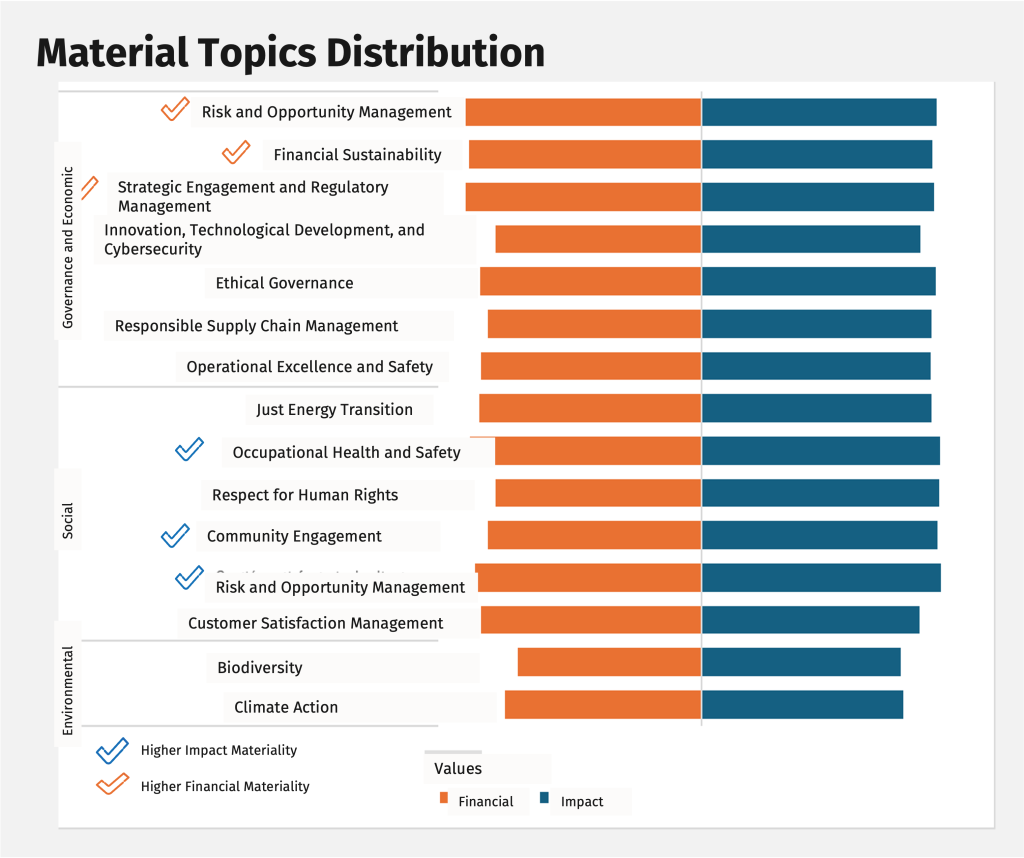

Material Topics Distribution

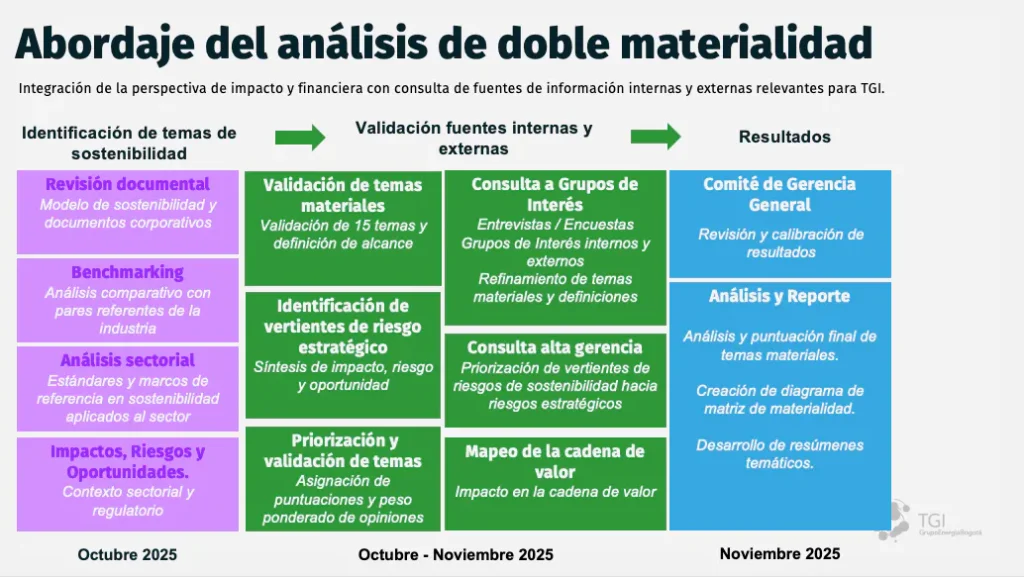

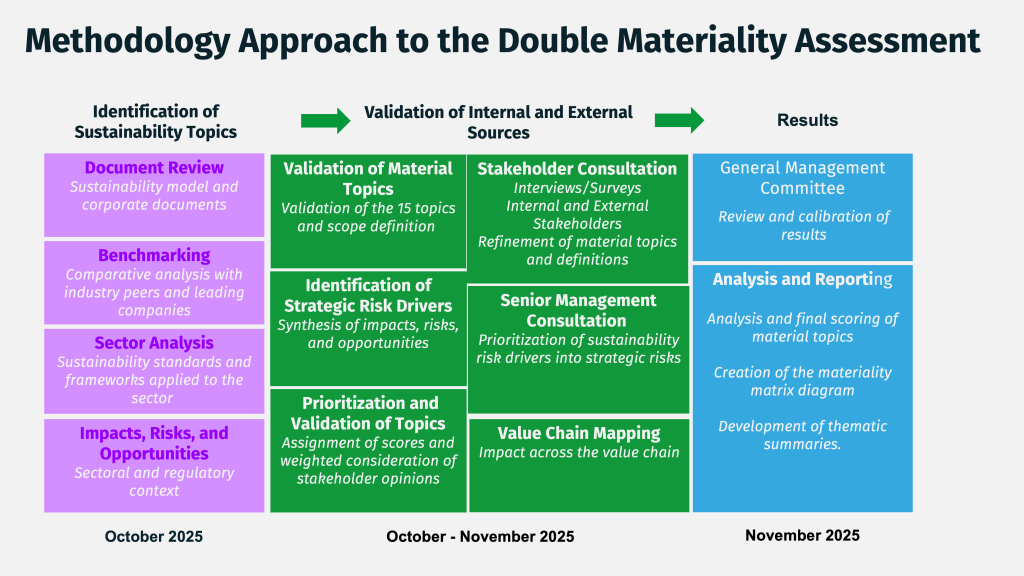

STAGES OF THE DOUBLE MATERIALITY ASSESSMENT

The stages carried out to determine double materiality are as follows:

Definition of Initial ESG Topics

Impact Materiality:

- Assessment of Potential Positive and Negative Impacts.

- Impact Assessment with Prioritized Stakeholders.

- Impact Materiality Results.

Financial Materiality:

- Financial Risk Assessment.

- Heat Map.

- Financial Materiality Results.

- Indicators with the Highest Impact.

Determination of Double Materiality Based on Methodological Criteria and Scoring Thresholds.

Methodology Approach to the Double Materiality Assessment

Integration of impact and financial perspectives through consultation with internal and externalinformation sources relevant to TGI.

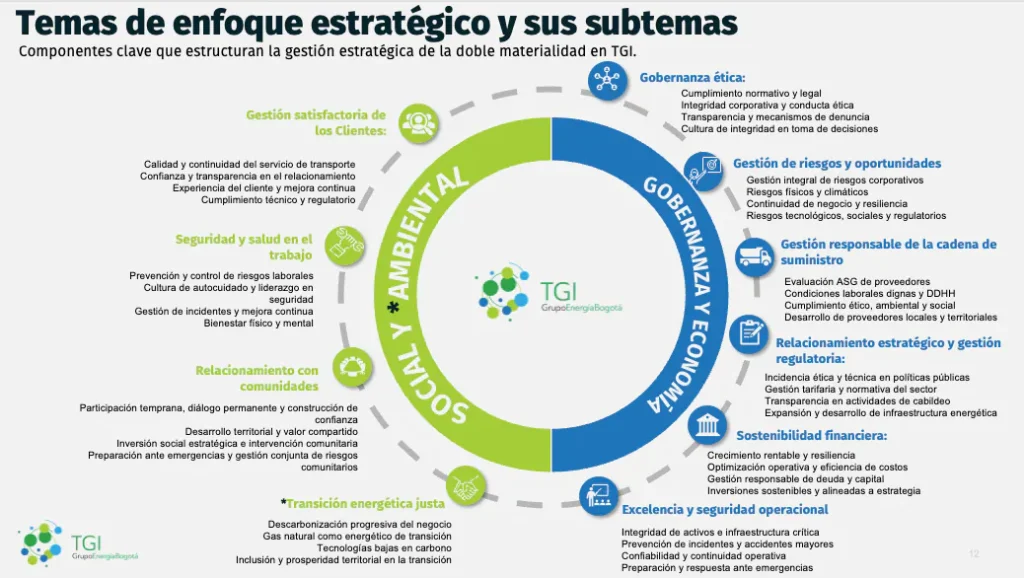

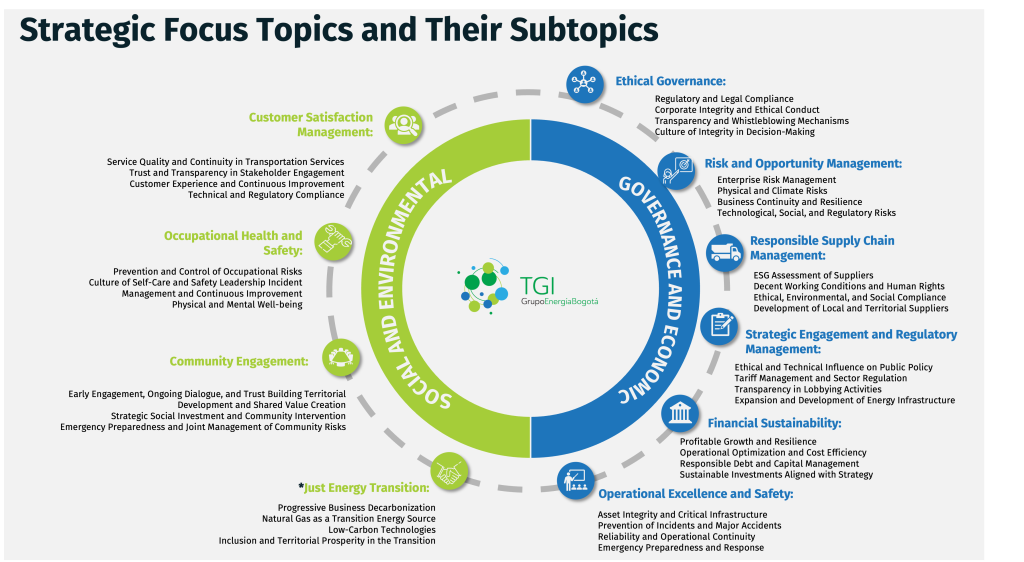

Strategic Focus Topics and TheirSubtopics

Key Components Supporting Double Materiality Strategic Management at TGI.

MATERIAL ISSUES FOR EXTERNAL STAKEHOLDERS

At TGI, we believe that open and constructive dialogue fosters development – both for the company and the communities within our area of influence. It also enables the success of our operational and expansion projects.

Conversely, the absence of transparent and effective dialogue may lead to social conflicts, mistrust, and opposition to projects, ultimately hindering local development and access to benefts.

Through our impact analysis, we also identified that failing to invest in building strong relationships with our stakeholders could result in the externalization of the cost of the «social license to operate,» triggering disruptive actions and reputational impacts that, in the end, compromise the well-being and stability of the communities we affect.

Download: 1.3.4 Impact valuation 2025[48] – Solo lectura